3 Failed Banks This Year Were Bigger Than 25 That Crumbled in 2008

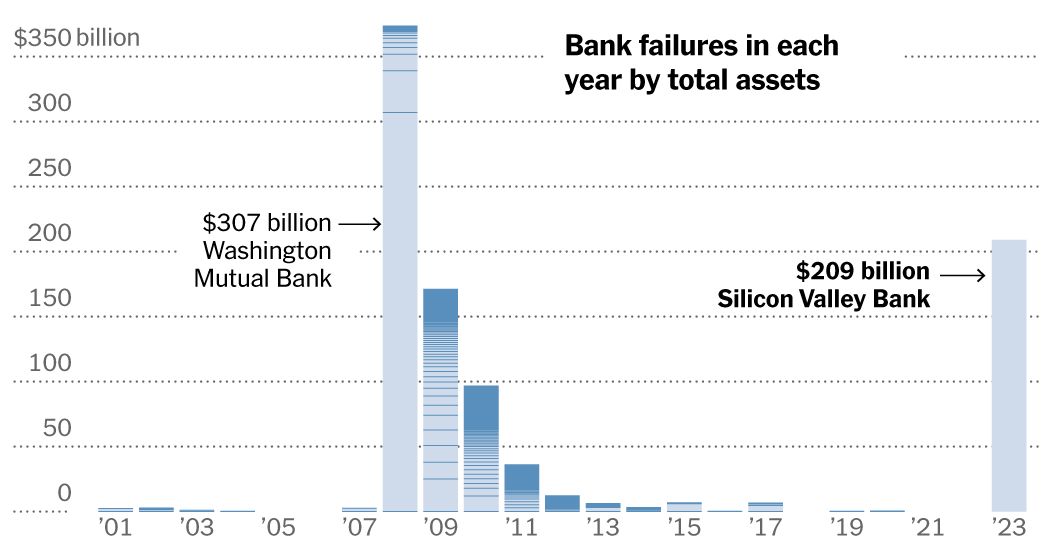

A bar chart of U.S. bank failures since 2001, showing that First Republic Bank’s collapse was the second-biggest in U.S. history in terms of assets. The three banks that failed this year were worth more in inflation-adjusted assets than the 25 that collapsed in 2008. Source: Federal Deposit Insurance Corporation Note: Chart includes failures of federally insured U.S. banks and does not include investment banks. By Karl Russell

Government regulators seized and sold off First Republic Bank on Monday, making it the third bank to fail this year after Silicon Valley Bank and Signature Bank collapsed in March.

The three banks held a total of $532 billion in assets. That’s more than the $526 billion, when adjusted for inflation, held by the 25 banks that collapsed in 2008 at the height of the global financial crisis.

The implosion of Washington Mutual that year, as well as the investment banks Lehman Brothers and Bear Stearns, was followed by failures throughout the banking system. From 2008 to 2015, more than 500 federally insured banks failed.

Most were small or midsize regional banks and were absorbed into other institutions, a common outcome for banks that have been put under government control. Washington Mutual, which was heavily involved in risky mortgages and became the largest bank to fail in U.S. history, was sold to JPMorgan Chase.

In recent years, fewer banks have gone under, thanks in part to stricter regulations that were put in place in the wake of the financial crisis. Before Silicon Valley Bank, the last bank to fail was in late 2020, as the coronavirus was ravaging the country.

The collapse of Silicon Valley and Signature Bank in March led to fears of fallout for the broader industry. Higher interest rates have eroded the value of assets on banks’ balance sheets, stressing the financial system and making it harder for banks to pay back depositors if they decided to withdraw their money.

A bar chart listing the top 30 U.S. banks by assets at the end of 2022. First Republic Bank ranks 14th, Silicon Valley Bank ranks 16th and Signature Bank ranks 29th. Source: Federal Reserve Board Note: As of Dec. 31, 2022. By Karl Russell

First Republic received a temporary $30 billion infusion from the nation’s biggest banks in March as a way to restore clients’ confidence. But customers pulled a staggering $102 billion in customer deposits over the first quarter of this year, according to the bank’s quarterly earnings report filed on Monday.

By the close of trading on Friday, the company’s stock price had dropped more than 75 percent this week.

Similar to Silicon Valley Bank, First Republic had many start-up industry clients, and many of its accounts held more than $250,000, the amount covered by federal insurance.

Top 50 banks by share of deposits that are not federally insured Excludes banking giants considered systemically important A bar chart showing the share of deposits that were not federally insured at 50 U.S. banks as of the end of last year. At both Silicon Valley Bank and Signature Bank, more than 90 percent of deposits were uninsured. At First Republic, this number was more than 67 percent. Greater share of deposits uninsured 25% 50 75 100 Silicon Valley 94% of $161 billion total deposits Signature 90% of $89 billion Bar heights are proportional to each bank’s total domestic deposits First Republic 68% of $176 billion Greater share of deposits uninsured 25% 50 75 100 Silicon Valley 94% of $161 billion total deposits Signature 90% of $89 billion Bar heights are proportional to each bank’s total domestic deposits First Republic 68% of $176 billion Sources: Federal Financial Institutions Examination Council; Financial Stability Board Notes: Data is as of Dec. 31, 2022. Includes domestic deposits only. Excludes global systemically important banks , which are subject to more stringent regulations, including tougher capital requirements. By Ella Koeze

The regulations put in place for the nation’s biggest banks after the financial crisis include stringent capital requirements, which means they must have a certain amount of reserves for moments of crisis, as well as stipulations about how diversified their businesses must be.

But midsize banks like First Republic, Silicon Valley and Signature do not have the same regulatory oversight. In 2018, President Donald J. Trump signed a law that lessened scrutiny for many regional banks. Silicon Valley Bank’s chief executive, Greg Becker, was a strong supporter of the move. Among other things, the law changed requirements for the amount of cash that these banks had to keep on their balance sheets to protect against shocks.

In a review of the Fed’s oversight of Silicon Valley Bank released on Friday, Michael S. Barr, the central bank’s vice chair for supervision, said the Fed would “re-evaluate” its rules for banks that were similar in size to Silicon Valley Bank.

Mr. Barr called the bank’s failure a “textbook case of mismanagement.” But he faulted Fed supervisors, too, for not understanding the extent of the bank’s vulnerabilities, and for failing to take decisive action when they did identify problems.

He also noted the real threat of contagion from Silicon Valley Bank. “A firm’s distress may have systemic consequences through contagion — where concerns about one firm spread to other firms — even if the firm is not extremely large, highly connected to other financial counterparties, or involved in critical financial services,” he wrote.

Source: The New York Times