Mortgage rates could soar to 8.4 percent if Biden does not stop a debt default, experts warn

Biden now 'considering' using the 14th Amendment to end debt showdown

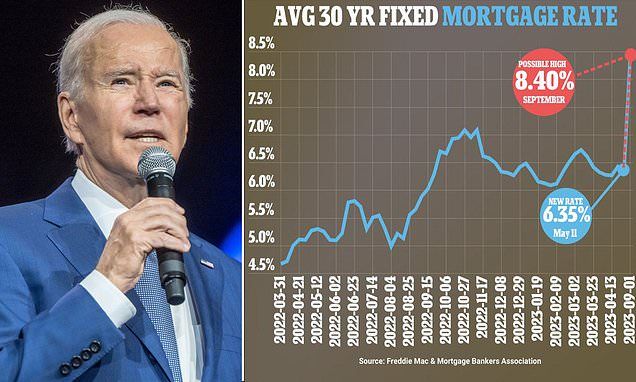

But experts say a debt default could see them shoot up to 8.4 percent

Mortgage rates fell to 6.35 percent this week, down from 6.39 the week before

Homeowners could see mortgage rates rocket to 8.4 percent if the US defaults on its debt, analysts have warned - after they fell to 6.35 percent this week.

President Joe Biden has less than one month to stop the country defaulting for the first time in history after Treasury Secretary Janet Yellen warned the Government may not be able to pay its bills by June 1.

If a solution is not reached, households face fiscal chaos which could cause seven million jobs to be lost and investments to plummet.

Now experts from property website Zillow have estimated that such an outcome could cause mortgage rates to soar as high as 8.4 percent by September.

This would push up the cost of an average mortgage repayment by 22 percent, Zillow warned.

Mortgage rates slipped to 6.35 percent this week - but experts said they could rocket to 8.4 percent if a debt default occurs

Today figures from lender Freddie Mac showed that the average rate on a fixed-rate 30-year mortgage was now 6.35 percent - down from 6.39 the week before.

Jeff Tucker, a senior economist at Zillow, said: 'Home buyers and sellers finally have been adjusting to mortgage rates over 6% this spring, but a debt default could potentially raise borrowing costs even higher and send the market into a deep freeze.

'Home values might not see a notable drop, but higher mortgage rates would severely impair affordability, for first-time buyers especially.'

He added that it was 'critically important' that lawmakers found a solution before a default occurs.

The threat of a default first emerged in January when the US hit its $31.4 trillion debt ceiling.

Since then the Treasury has been using what it describes as 'extraordinary measures' to keep its balance books afloat.

But on Monday Treasury Secretary Janet Yellen warned that the Government may not be able to pay all of its bills on time by as soon as June 1.

It has led to panic from both sides of the political spectrum.

On Monday Biden went to toe-to-toe with Republican speaker Kevin McCarthy in their first meeting in over three months.

The two men are entrenched in opposing views as Biden wants to raise the debt ceiling to stop a default.

However McCarthy has insisted the measure will not pass through Congress.

A debt default could see social security payments delayed, investments drop and mortgage rates soar

Biden expressed similar reservations about using the 14th Amendment when discussing the option with journalists Tuesday night

Biden is now 'considering' using the 14th Amendment to push through an increase to the debt ceiling - though he expressed reservations about doing so.

The 14th Amendment says 'the validity of the public debt, authorized by law... shall not be questioned.'

However today Yellen condemned the idea as 'legally questionable.'

The revelation comes after homeowners appeared to have some respite from soaring mortgage rates which first went above 6 percent since September.

In recent weeks they have appeared to stabilize, with rates hovering just below the 6.5 percent mark.

This time last year the average rate on a 30-year fixed-rate mortgage was 5.3 percent.

After dropping again this week, Freddie Mac's Chief Economist Sam Khater said: 'This week’s decrease continues a recent sideways trend in mortgage rates, which is a welcome departure from the record increases of last year.

'While inflation remains elevated, its rate of growth has moderated and is expected to decelerate over the remainder of 2023.

'This should bode well for the trajectory of mortgage rates over the long-term.'

Source: Daily Mail